If you’re new to the business world, you might ask what is a sole proprietorship. It is the simplest form of business that you can run individually. Here a single person manages, controls, and operates the business affairs. The person who runs such a business is called a sole trader or sole proprietor. Before going into the depth of sole proprietorship, you should first know what is a sole proprietorship. Let’s find out all.

What is Sole Proprietorship?

A Sole proprietorship is a business that can’t be considered a legal entity and it doesn’t need to be incorporated to the companies house. In a sole proprietorship, the sole trader and business are considered one body. It has unlimited liability, where your personal possessions are at risk. According to the estimate of 2020, there are more than 75% of the people in the UK who’re engaged in this type of business.

The sole proprietor has to pay personal income tax from the turnover of the business. Compared to others, it’s the easiest type of business as it needs less capital, less human resources and there are almost no legal regulations on it.

Want to start a business but don’t know where to start. Reach out to our specialist for help.

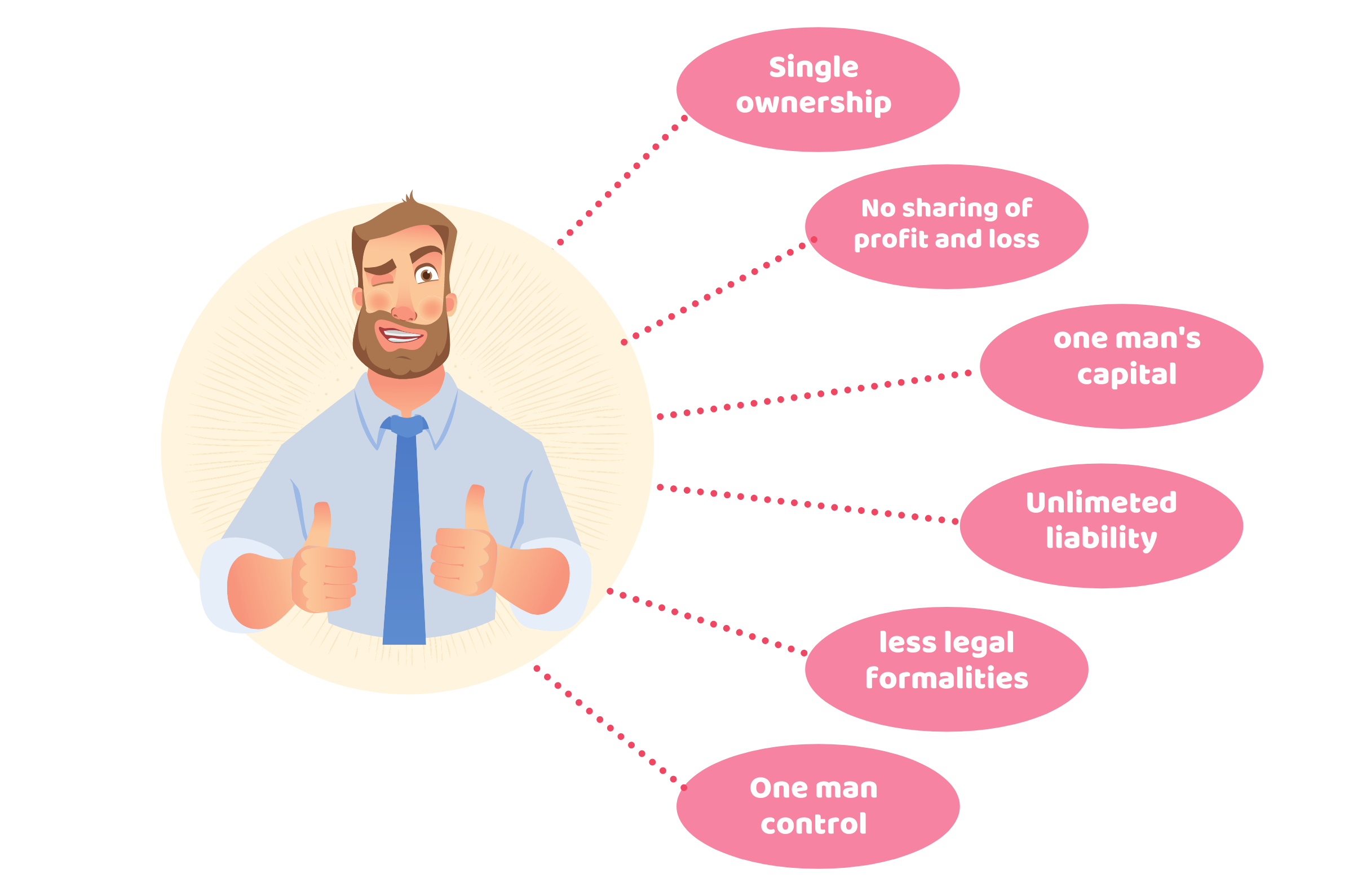

Characteristics of Sole Proprietorship:

1- Sole Ownership:

Here the person has sole ownership over his business. All the assets are the personal property of the sole proprietor. He is the key decision-maker for his business. He has the authority to dissolve the business or the business might end at his demise.

2- No Profit and Loss Sharing:

If a business is booming with a lot of profit, only the owner will enjoy it. Similarly, if there is any loss, he’s the sole bearer of that loss.

3- Singlehanded Capital:

The sole proprietor brings the capital to the business on his own without the help of any other person. He can generate capital by personal assets or by borrowing from relatives, friends, banks, financial institutes etc.

4- One Man Control:

Unlike other business types, sole proprietors have full-fledged control of the business. The owner can do whatever he wants for the business as per his personal choice.

5- Less Legal Requirements:

This business contains fewer legal requirements. It doesn’t have any registration fees to open and close the business.

6- Unlimited Liability:

It is one of the disadvantages of a sole proprietorship that the liability is unlimited. Your personal and business assets are considered the same. Thus at the time of need or emergency, your personal assets can be used to pay the liabilities of the business.

If you want to start a business, let us know for assistance.

Merits of Sole Proprietorship:

It is one of the oldest, simplest, and easiest types of business where one person has the sole control of all business affairs. Some common examples include; shops, barbers, parlours, workshops, etc.

- Easy to open and close

- Maintenance and business secrets

- Singlehanded control

- Quick decision making and planning

- Least legal requirements and records

- Personal relation

Demerits of Sole Proprietorship:

- Limited Resources

- Confined managerial activities

- Limited Time

- Unlimited liability

- Small Size

Quick Sum Up:

So you’ve got the answer to what is a sole proprietorship. Despite many limitations, most business owners, especially startups, prefer this business type as it is simple, easy, and requires low capital. This business is useful if there is a demand for personalized products or services. It is best for those businesses where manual skills and expertise are employed with small capital and fewer risks.

Want to work like an online sole trader providing accounting services across the UK, register now on accounting firms for free to earn!

Accounting firms is the best accounting and taxation business listing website in the UK. Contact us anytime.

Disclaimer: It is an informative blog proving the basic information on sole proprietorship.